The standard UPI transaction limit 2026 is 1 lakh per day for most users, covering both person-to-person and merchant payments, and this cap applies across all your UPI apps combined, not per app.

Author: Aadarsh Patel | EQMint

Most banks also cap you at around 20 UPI transactions a day. Certain categories go far higher: payments for IPOs, capital markets, insurance, education, healthcare, tax and government services can go up to 5 lakh per transaction.

UPI Lite runs as a separate small-payment wallet that does not count toward the 1 lakh limit. And the biggest change coming is mandatory two-factor authentication on every digital payment from April 1, 2026.

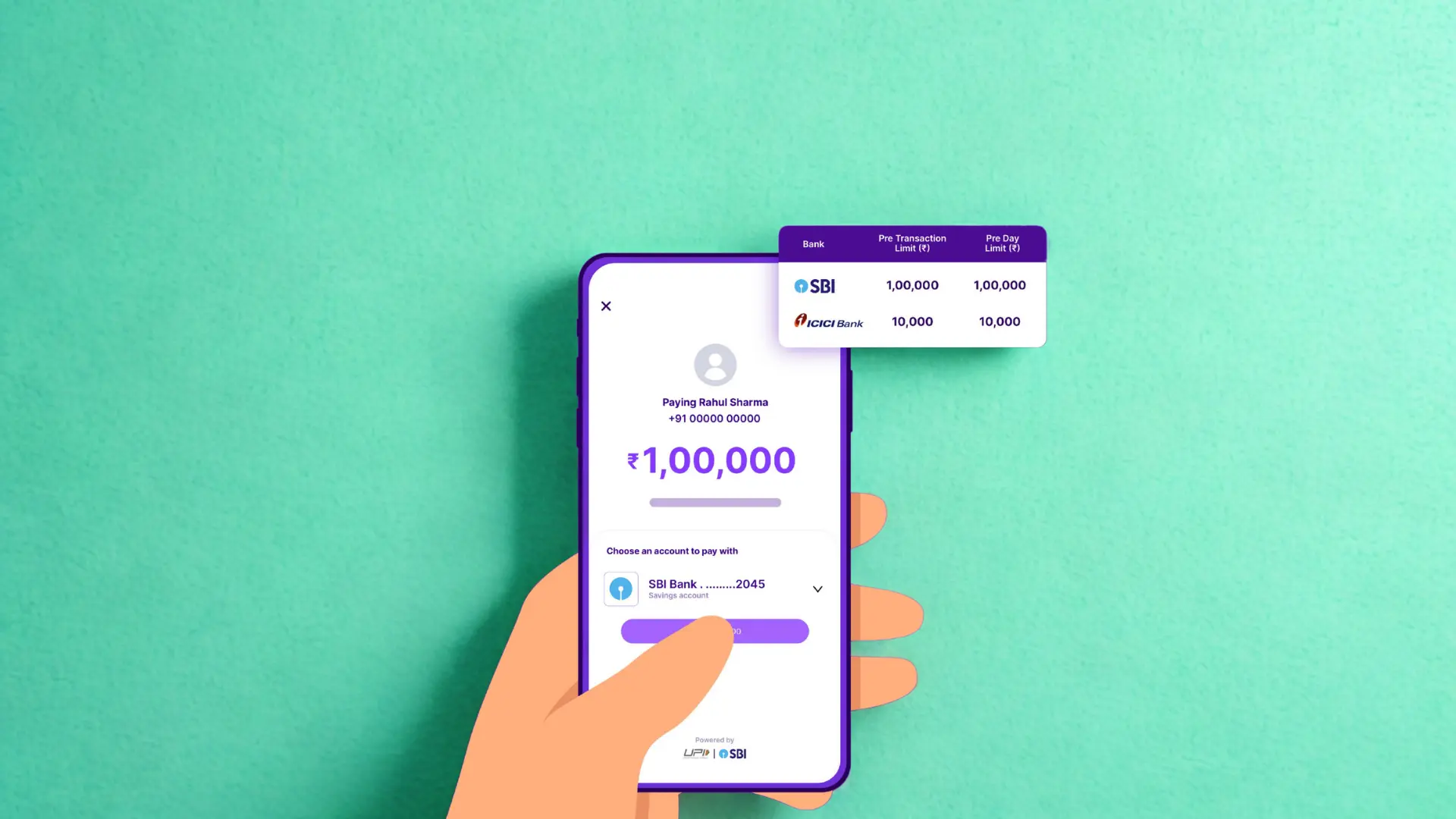

The headline number people search for, 1 lakh, is a ceiling set by NPCI, not a guarantee. Your own bank can set it lower based on its risk rules, which is why two people on the same app can have different limits.

Here’s the full, current picture of UPI limits in 2026, the special category caps, the new features and exactly what’s changing.

The standard UPI transaction limit 2026, explained

Start with the number that matters most. NPCI sets the standard daily UPI limit at 1 lakh, and it works as a combined ceiling across everything you do on UPI.

Two details trip people up. First, the 1 lakh cap is aggregate across all your UPI apps tied to the same bank account, so using PhonePe, Google Pay and Paytm together doesn’t multiply your limit. Second, most banks add a count cap of around 20 transactions per 24 hours, measured on a rolling window from your first transaction of the day. Hit either the value or the count ceiling and further payments are blocked until the window resets.

And the bank has the final say. NPCI sets the upper limit, but your bank can set a lower one, anywhere from 25,000 to 1 lakh depending on the bank, your account type and history. If a payment fails under 1 lakh, your bank’s own cap is often the reason.

The higher category limits, up to 5 lakh

This is the part many people don’t know, and it’s genuinely useful. For specific verified categories, NPCI allows much higher per-transaction limits, up to 5 lakh, effective from September 2025.

| Payment type | Higher limit |

| IPO (ASBA) and capital markets | Up to 5 lakh per transaction |

| Insurance premiums | Up to 5 lakh per transaction |

| Education and healthcare (verified) | Up to 5 lakh per transaction |

| Tax and government payments | Up to 5 lakh per transaction |

| RBI Retail Direct scheme | Up to 5 lakh per transaction |

A practical tip worth knowing. These higher limits depend on the merchant being correctly registered under the right NPCI category. So if a hospital or college bill above 1 lakh fails, the problem is usually the merchant’s category registration, not your own limit. There’s little you can do from your side except ask the institution to check, or pay another way.

UPI Lite, 123Pay and the smaller rails

UPI is not one single pipe. Several variants run alongside it with their own limits, built for different needs.

UPI Lite. An on-device wallet for small, frequent payments, with no UPI PIN needed below the cap. The per-transaction limit was raised to 1,000 and the maximum wallet balance to 5,000. Its big advantage: UPI Lite spending does not count toward your 1 lakh daily limit, so it acts as a parallel rail for chai-and-bus-ticket payments and even works offline up to a 5,000 total.

UPI 123Pay. For feature phones with no internet, working through IVR, missed calls and OEM apps. The per-transaction limit is 10,000, important for financial inclusion in low-connectivity and rural areas.

Using UPI Lite for routine small spends is a quietly smart move, because it keeps your main 1 lakh limit free for the payments that actually need it.

The new-user and safety caps

Several limits exist purely to fight fraud, and they catch new users off guard.

When you first register a UPI ID or link a new bank account, many banks cap you at around 5,000 total in the first 24 hours. It’s a cooling-off measure against fraud, and the limit rises as your account builds a history. Beyond that, NPCI has added a set of system-health caps: you can check your balance up to 50 times per day per app, link up to 25 accounts per day per app, and check a pending transaction’s status only 3 times with a mandatory 90-second gap between checks. These exist to stop apps overloading the banking servers, which used to cause outages at peak times.

What is changing in 2026

Here’s the forward-looking part, the actual changes rolling out. Most are about safety and stability rather than new limits.

Mandatory two-factor authentication, April 1, 2026. The biggest change. Under RBI’s 2025 authentication directions, every domestic digital payment, including UPI, must use two authentication factors from different categories, with at least one dynamic factor per transaction. A static UPI PIN or an SMS OTP alone will no longer be enough. Expect biometrics, secure in-app approvals and extra checks on high-risk payments. The aim is to kill fraud built on stolen static credentials.

Payee name display. Apps now show the verified, bank-registered name of whoever you’re paying, instead of a self-set nickname, so you can confirm you’re sending money to the right person before you tap pay. A simple, strong anti-fraud step.

Auto-debit in off-peak windows. Recurring payments like SIPs, EMIs, credit card bills and subscriptions are now processed in designated non-peak windows, broadly before 10 AM and after 9:30 PM, to ease congestion and improve success rates. Your autopay still works, it just runs in the background at quieter times.

The 30% market-share cap, deferred to December 31, 2026. NPCI’s long-planned rule to cap any single app at 30% of UPI volume has been pushed back again. For now PhonePe and Google Pay remain well above that, but expect gentle nudges toward smaller apps over time.

Other developments are on the way too, faster settlement in the background, AI-assisted help within apps, Aadhaar face authentication, real-time PIN reset, and UPI’s continued expansion to more countries through tie-ups and Project Nexus. None of these change your daily limit, but they reshape the experience.

UPI limits at a glance

The quick reference, all the key 2026 numbers in one place.

| Limit type | 2026 figure | Note |

| Standard daily | 1 lakh | Across all apps combined |

| Transaction count | ~20 per day | Set by your bank |

| Special categories | Up to 5 lakh | Per transaction, verified |

| UPI Lite per payment | 1,000 | Doesn’t count to 1 lakh |

| UPI Lite wallet | 5,000 | On-device, no PIN |

| UPI 123Pay | 10,000 | Feature phones |

| New user, first 24h | ~5,000 | Fraud cooling-off |

Does UPI cost anything in 2026?

For normal use, no. Bank-to-bank UPI payments remain free for individuals, both P2P and P2M. That hasn’t changed and there’s no consumer charge on a standard UPI transfer.

The one nuance is wallet-based (PPI) payments, where an interchange fee of roughly 0.5% to 1.1% applies on certain merchant transactions above 2,000, but that fee is paid by the merchant, not by you. And UPI itself creates no tax. Money you receive is only taxable if it’s actually income or business revenue, which UPI simply makes traceable. A personal transfer between friends or family is not taxed for being sent over UPI.

FAQ

What is the UPI transaction limit per day in 2026?

The standard limit is 1 lakh per day for most users, covering both P2P and merchant payments, applied across all your UPI apps combined. Many banks also cap you at around 20 transactions per day.

Can I send more than 1 lakh through UPI?

Yes, for specific verified categories. Payments for IPOs, capital markets, insurance, education, healthcare, tax and government services can go up to 5 lakh per transaction, effective from September 2025.

Does using multiple UPI apps increase my limit?

No. The 1 lakh daily limit is aggregate across all UPI apps linked to the same bank account, so using several apps does not multiply your available limit.

Why did my UPI payment fail even though it was under 1 lakh?

Often because your bank sets a lower limit than the NPCI ceiling, or you hit the daily transaction count cap. For large category payments, the merchant’s NPCI category registration may also be the issue.

What is UPI Lite and what is its limit?

An on-device wallet for small payments with no UPI PIN needed below the cap. It allows up to 1,000 per transaction and a 5,000 wallet balance, and importantly its spending does not count toward your 1 lakh daily limit.

What is changing in UPI from April 2026?

From April 1, 2026, every domestic digital payment including UPI must use two-factor authentication with at least one dynamic factor. A static UPI PIN or SMS OTP alone will no longer be sufficient, with biometrics and secure in-app approvals expected.

Are there charges on UPI payments in 2026?

No, for normal bank-to-bank UPI payments by individuals. A small interchange fee applies only to certain wallet-based merchant transactions above 2,000, and that is paid by the merchant, not the customer.

Is money received through UPI taxable?

UPI itself creates no tax. Money is taxable only if it is income or business revenue, which UPI makes traceable. A personal transfer between friends or family is not taxed simply for being sent over UPI.

EQMint is not a SEBI registered investment adviser. This article is for informational purposes only and is not investment or tax advice. UPI limits, features and rules are set by NPCI and individual banks and change frequently, so always confirm current limits with your bank or UPI app before relying on them.

For more such information visit EQMint

Join our Whatsapp channel for timely updates: Whatsapp